HOA & Condo Communities: Understanding Your Financial Reports

Many homeowners and board members find themselves looking at financial reports only to realize that they do not understand what they are looking at. Truth is, not all of us have experience or education in reviewing numbers and reports. If you are a Board Member though, it is your fiduciary responsibility to oversee the financial health of your community, making sound and diligent decisions with your homeowner’s money. You may receive many monthly reports from your Management Company, but let’s review the top five most important, what they mean and potential watch outs.

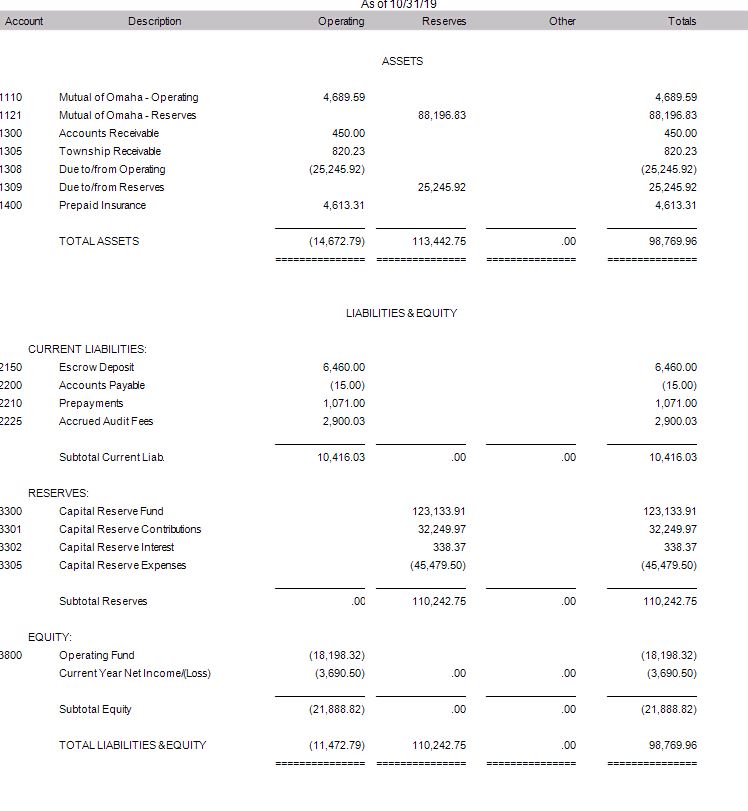

The Balance Sheet

For many reasons the Balance Sheet is the most important and truest review of the financial health of your association. The Balance Sheet shows the bank balances in all bank accounts, including reserve and working capital accounts, loan balances, accounts receivable (money owed the association), prepaid expenses, reserves and equity growth/loss. If you are practicing Fund Management (which most property management companies should be doing as best practices), the columns represent your different bank or investment accounts such as operating account (checking), reserve account (savings) and/or a working capital account (savings for capital projects). The rows represent your assets (positive wealth) and your liabilities (negative wealth).

For many reasons the Balance Sheet is the most important and truest review of the financial health of your association. The Balance Sheet shows the bank balances in all bank accounts, including reserve and working capital accounts, loan balances, accounts receivable (money owed the association), prepaid expenses, reserves and equity growth/loss. If you are practicing Fund Management (which most property management companies should be doing as best practices), the columns represent your different bank or investment accounts such as operating account (checking), reserve account (savings) and/or a working capital account (savings for capital projects). The rows represent your assets (positive wealth) and your liabilities (negative wealth).

Assets include balances in your bank accounts to date, money owed you from your homeowners, money owed from other vendors and expenses you have prepaid such as project deposits or property insurance.

Liabilities include payables (money you owe other vendors), accrued expenses (expenses not yet paid but anticipated)and loan balances.

Reserves highlight how much you have contributed into or taken out of your reserve (savings) fund. Reserve interest earned is also reflected there. Also, capital project expenses may also be taken directly from this account.

Equity represents whether, as of the date, you either had gained or loss financial worth as an association. On a balance sheet the Total Assets and Total Liabilities must always equal, thus the equity is used to balance the two…and is either positive (gained wealth) or negative (lost wealth).

Watch Outs! include:

- If your operating bank account is continually too low (not enough money to pay your bills).

- If your accounts receivable is too high (homeowners are delinquent on their payments).

- Not enough money is going into the reserve fund (it is important to save for future projects).

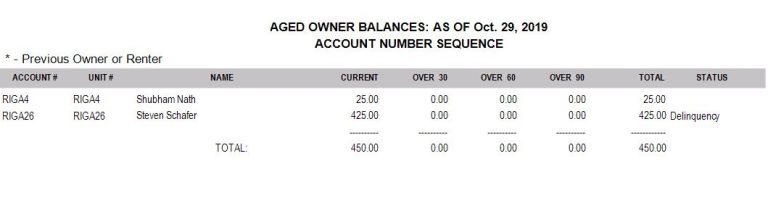

Accounts Receivable Report

When your Accounts Receivable line on the balance sheet is too high, it becomes important to review you’re A/R Aging Summary Report and see which homeowners are delinquent in their monthly payments. Your maintenance dues are your primary source of income, so it is important to stay on top of your overdue owners and take firm and consistent action to collect. Your Property Management Company should have procedures in place, such as late letters, email/phone calls and eventually attorney lien/eviction procedures in place to help you manage.

When your Accounts Receivable line on the balance sheet is too high, it becomes important to review you’re A/R Aging Summary Report and see which homeowners are delinquent in their monthly payments. Your maintenance dues are your primary source of income, so it is important to stay on top of your overdue owners and take firm and consistent action to collect. Your Property Management Company should have procedures in place, such as late letters, email/phone calls and eventually attorney lien/eviction procedures in place to help you manage.

Watch Outs! include:

- All homeowners over 60 days delinquent

- All 120-day delinquencies are with an attorney and have property liens in place. These liens should be updated every 6-12 months.

- Attorneys should provide the Board with a monthly status report ensuring legal actions are continuing to move forward. Dead beats are expensive for an association to deal with and take time to evict, obtain bank or wage garnishments or rent receiverships. It is important that the lawyers are moving as quickly as possible when their services are needed

Bank Reconciliation

The Bank Reconciliation report is used to prove that your checking account ‘cash asset’ shown on the Balance sheet agrees with what the bank account reflects. It is important to understand the monies flowing into and out of your operating and reserve accounts each month. Additionally, it helps ensure that your Property Management Company is paying invoices in a timely fashion.. If you are not given actual invoices each month, request them and review. For example, make sure the landscape costs are reasonable and within the scope of your contract, the insurance premium, gas, electric and water are getting paid each month

Watch Outs! include:

- Consistent late fees.

- Invoice amounts and checks do not match (which could mean your property management is padding the invoices).

- Missing monthly invoices like gas or electric.

- Uncashed checks laying on your books for too long.

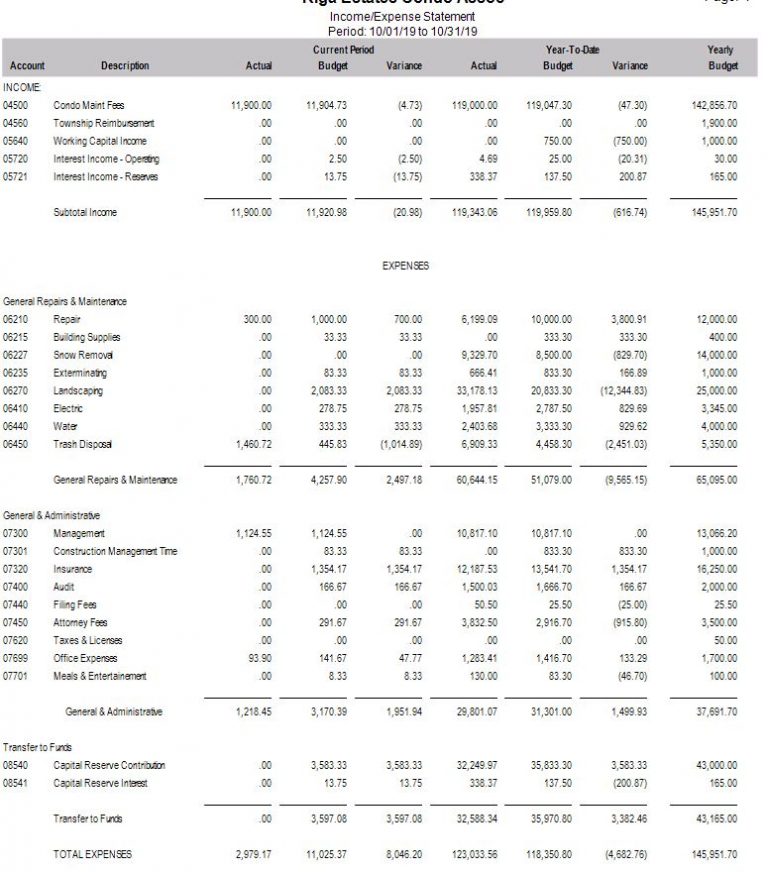

Income Statement

Most Board Members and Homeowners think the Income Statement, otherwise known as a Profit and Loss Statement, is the MOST important report. The Income Statement allows you to monitor your monthly expenses compared to income and helps you understand how you are doing in relationship to your budget. If there are large discrepancies between your actual spending and your budget, it flags a potential problem and forces you to dig deeper and make spending decisions. For example, you may have an exceptionally cold winter and spend more on snowplow. Your options may to be to either borrow monies from reserves, cut expenses in other areas or assess your homeowners to make up the difference. Another important note is that these financial statements can be prepared in two different ways, on a Cash Basis and on an Accrual Basis. It is important to understand the difference between the two and which you are looking at, however, best practices dictate accrual accounting is the industry standard.

Most Board Members and Homeowners think the Income Statement, otherwise known as a Profit and Loss Statement, is the MOST important report. The Income Statement allows you to monitor your monthly expenses compared to income and helps you understand how you are doing in relationship to your budget. If there are large discrepancies between your actual spending and your budget, it flags a potential problem and forces you to dig deeper and make spending decisions. For example, you may have an exceptionally cold winter and spend more on snowplow. Your options may to be to either borrow monies from reserves, cut expenses in other areas or assess your homeowners to make up the difference. Another important note is that these financial statements can be prepared in two different ways, on a Cash Basis and on an Accrual Basis. It is important to understand the difference between the two and which you are looking at, however, best practices dictate accrual accounting is the industry standard.

CASH BASIS is the easiest to understand. It simply reports the cash income you have receive (mostly maintenance fee income) and what you pay in expenses. The difference between the two is your profit or loss.

ACCRUAL BASIS. This method is a little more complicated. Accrued accounting takes ‘anticipated (not actual) income and expense’ and spreads it evenly over the twelve months. This method assumes that the monies collected (maintenance fees) and annual expenses (like insurance) are paid and collected evenly all year. Maintenance fee income, insurance, bad debt allowance and reserve savings are the most common line items that are accrued. Most others are on a cash basis.

BUDGET COMPARISON is the most important thing to review on the Income Statement. A good budget is developed at the end of the previous year. It should cover anticipated expense, increases, projects and reserve savings. A good budget starts by estimating all future year expenses. Then, the maintenance fees are calculated to cover these expenses. This ‘bottoms up’ approach helps avoid assessments throughout the year. It also is your roadmap to maintain or improve your Balance Sheet (the financial health of the association). Once the budget is in place, you can track how you are doing each month and year-to-date.

Watch Outs! include:

- Large variances between actual expense and budget. Ask why?

- If your Expenses are projected to exceed your Income by year end.

Capital Reserve Plan

A Capital Reserve Plan is a report that needs to be reviewed annually. Planning for future projects is essential to maintaining the value of your largest investment, your home. Capital projects such as new roofs, furnaces, windows, decks etc.… are often large expenses that if not properly planned for can wipe out an association financially. Additionally, proper reserve planning is important when securing competitive insurance rates and for refinancing your own individual mortgages.

As a volunteer board member, a large part of your responsibility is your fiduciary responsibility to the community. Overseeing the monies of your homeowners, ensuring they are safe and being spent responsibly is extremely important. Take time each month to review these reports and ask questions of your Treasurer or Property Manager. As an involved homeowner, ask these same questions of your Board. Denali Property Management provides these reports, and more, each month. Our property managers are trained in financial analysis and are supported with a team of professional bookkeepers and accountants.